HSA vs FSA, Understanding the Key Differences

Key Takeaways

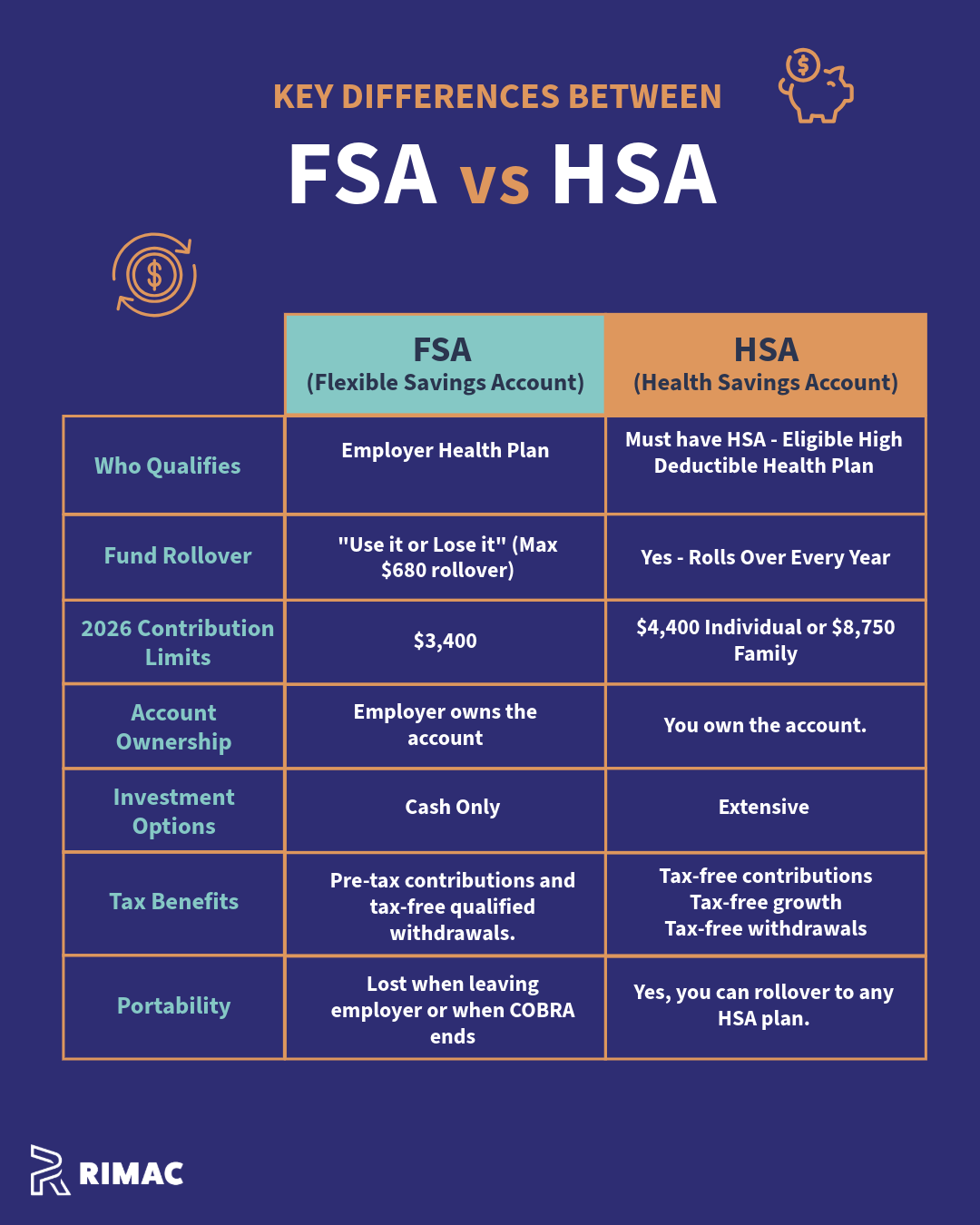

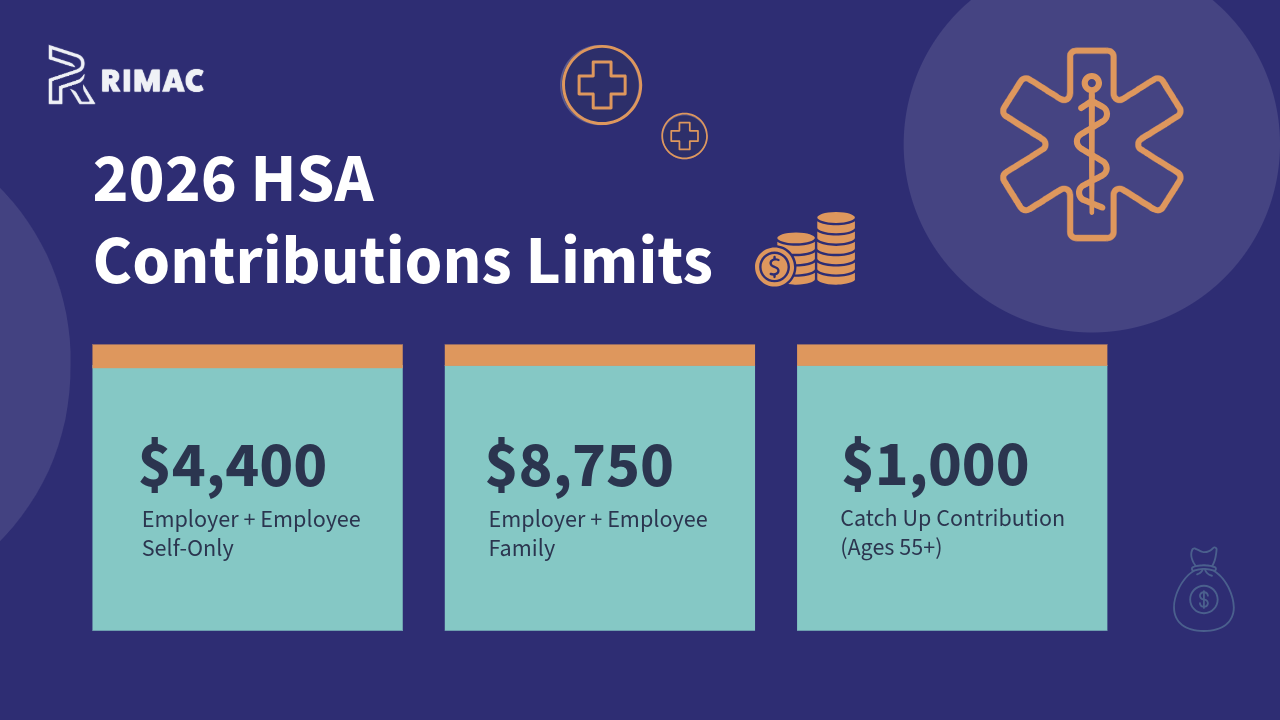

For 2026, the maximum HSA contribution is $4,400 for individuals and $8,750 for families. The maximum contribution for an FSA is $3,400.

Those aged 55 and older can contribute an additional $1,000 to an HSA

Tax-advantaged healthcare accounts like HSAs and FSAs are powerful tools for managing medical expenses while lowering your taxable income. Both offer meaningful savings, but differences in structure, eligibility, flexibility, and long-term value mean that one may be a better fit depending on your situation.

What are HSAs and FSAs?

Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) are designed to help you pay for qualified medical expenses using pre-tax dollars. By reducing your taxable income and allowing tax-free withdrawals for eligible costs, they can significantly lower the overall cost of healthcare.

Health Savings Account (HSA)

A Health Savings Account is available to individuals enrolled in a qualified high-deductible health plan. Contributions are made with pre-tax dollars, the account grows tax-free, and withdrawals used for eligible medical expenses are also tax-free. This triple tax advantage makes HSAs uniquely powerful.

One of the defining features of an HSA is ownership. Even if the account is opened through your employer, the HSA belongs to you. The balance rolls over from year to year with no expiration, and unused funds can be invested for long-term growth. Over time, this transforms the HSA from a simple spending account into a strategic savings vehicle for future healthcare expenses.

Flexible Spending Account (FSA)

A Flexible Spending Account is an employer-sponsored benefit that also allows you to set aside pre-tax dollars for qualified healthcare expenses. FSAs are often easier to access because they are not tied to a specific type of health plan.

However, FSAs come with stricter rules. The account is owned by your employer, not you, and unused funds are generally forfeited at the end of the plan year unless your employer offers a limited rollover or grace period. FSAs also do not offer investment options, so balances remain in cash.

Source: Rimac Capital

Contribution Limits and Employer Contributions

Both HSAs and FSAs are subject to annual contribution limits set by the IRS, and those limits are adjusted periodically. Employers may also set their own FSA limits, as long as they remain within IRS guidelines.

In general, HSA contribution limits are higher than FSA limits, and individuals age 55 and older may make additional catch-up contributions to an HSA. If your employer contributes to your HSA or FSA on your behalf, those amounts count toward your annual limit and may reduce how much you can contribute personally.

Because these limits can change from year to year and may be affected by employer funding, it is important to review your plan details carefully before making elections.

Contribution Limits:

For 2026, HSA contribution limits are $4,400 for individuals and $8,750 for families, with an additional $1,000 catch-up contribution allowed for those age 55 and older.

For 2026, FSA contribution limits are $3,400 for individuals. At the end of the year, up to $680 may be rolled over if your employer allows it. Contributions can typically be adjusted during open enrollment or following certain life events, such as a change in family status, plan selection, or employer.

Source: Rimac Capital

Can You Have an HSA and an FSA at the Same Time?

In most cases, you cannot contribute to both a standard healthcare FSA and an HSA in the same year. The IRS does not allow overlapping tax benefits for the same category of medical expenses.

That said, there is an important exception. If your employer offers a limited purpose FSA, you can contribute to that account while also funding an HSA. A limited purpose FSA is restricted to expenses not typically covered by your health plan, most commonly dental and vision care.

This restriction does not apply to dependent care FSAs. You can contribute to an HSA and a dependent care FSA in the same year without issue.

Ownership and Portability Matter

One of the most significant differences between these accounts becomes apparent when you change jobs.

An HSA is yours permanently. You keep the account and its balance even if you leave your employer, change health plans, or stop working altogether. In certain situations, HSA funds can also be used to pay for COBRA coverage or health insurance premiums while unemployed.

An FSA, by contrast, is tied to your employer. If you leave your job, any remaining balance is typically forfeited unless you elect COBRA coverage and continue contributing. This lack of portability makes FSAs far less flexible over time.

Access to Funds During the Year

FSAs offer a short-term cash flow advantage that can be useful for predictable medical expenses. The full amount you elect to contribute for the year is available on the first day of your plan year, even though contributions are deducted from your paycheck over time.

HSAs work differently. Funds are only available as contributions are made. If you contribute gradually throughout the year, your available balance may be limited early on.

However, HSAs offer an important workaround. You can pay for a qualified medical expense out of pocket, save the receipt, and reimburse yourself later once your HSA balance has grown. This flexibility allows HSAs to function similarly to FSAs while preserving their long-term advantages.

Investment Potential and Long-Term Value

HSAs stand apart because they allow unused balances to be invested once a minimum cash threshold is met. Over time, investment growth can significantly increase the value of the account, particularly for those who do not need to spend their HSA funds each year.

FSAs do not offer investment options. Funds remain in cash and are generally intended to be used within a relatively short time frame.

What Happens at Age 65?

Before age 65, using HSA funds for non-qualified expenses generally triggers income taxes plus a 20 percent penalty. After age 65, that penalty is eliminated.

At that point, an HSA begins to function similarly to a traditional retirement account. Withdrawals used for non-medical purposes are taxed as ordinary income, much like a traditional IRA or 401(k). Withdrawals for qualified medical expenses remain tax-free.

This makes the HSA one of the most tax-efficient tools available for planning future healthcare costs in retirement.

Which Account Is Right for You?

An HSA may be a strong fit if you are enrolled in a high-deductible health plan, value flexibility, and want long-term tax-advantaged savings. For those who can afford to let balances grow, the HSA can play a meaningful role in retirement planning.

An FSA may be more appropriate if you have predictable medical expenses, want immediate access to funds, or are not eligible for an HSA. When used carefully, an FSA can still provide meaningful tax savings within a single plan year.

Final Thoughts

HSAs and FSAs both offer valuable tax advantages, but they serve different purposes. The right choice depends on your health plan, expected medical spending, job stability, and long-term financial strategy.

Taking the time during open enrollment to understand these differences can help you maximize tax savings while avoiding costly mistakes. Used thoughtfully, either account can be a powerful complement to your overall financial plan.

At Rimac Capital, we help clients evaluate options like HSAs and FSAs within the context of their broader financial picture, ensuring healthcare decisions align with cash flow needs, tax efficiency, and long-term planning goals.

Connect with Us Today

Schedule a free 30-minute consultation call. We’ll learn more about your priorities and ensure we can answer all of your questions.